Get your Geek on with Electronics Notes

Electronics Notes has been continuing to develop its online shop and is starting to broaden out the product range.

One key product being introduced is downloadable PDF eBooks. Currently, three books are available covering:

A Guide to Operational Amplifiers: This book introduces the fundamentals of operational amplifiers and explores their practical applications in circuits such as amplifiers, filters, oscillators, integrators, and differentiators and more.

A Guide to the Superheterodyne Radio: This book explores the invention, operation, circuit blocks, and specifications of superheterodyne radios and their impact on overall performance.

A Guide to Digital and Analogue Multimeters: This book provides a basic introduction to the operation, specifications, and practical use of multimeters for engineers, technicians, hobbyists, and others.

Due to popularity, there are plans to increase the number of books that are available in the future, so it is worth checking back to find out more.

Visit the Electronics Notes online shop to find out more: https://electronics-notes-shop.fourthwall.com/collections/ebooks

Microelectronics UK Set for September Launch at ExCeL London

A new event, Microelectronics UK, will debut on 24th–25th September 2025 at ExCeL London, bringing together the UK’s microelectronics, semiconductors, photonics, and embedded systems communities in one place.

The show will feature exhibitions, conference sessions, workshops, and product showcases, with over 100 exhibitors and thousands of visitors expected. Key segments include a Start-Up Launchpad for innovators and a dedicated Skills Zone created to tackle the sector’s growing talent gap.

By uniting industry leaders, researchers, and start-ups, Microelectronics UK aims to strengthen collaboration across businesses and highlight the UK’s role in the industry.

It's great to see the launch of new events that shine a light on specific sectors within the industry. We look forward to hearing about the feedback from the show.

Registration is now open for the show, and further information can be found by clicking here.

Electronics AI Summit Taking Place November 2025

Talking IoT has announced an Electronics in AI Summit, a three-day virtual gathering, taking place from11th, 12th-13th of November 2025.

Hosted by Talking IoT and GenAI Nerds, the summit invites global innovators and leaders to share how advances in electronics are powering and enabling the future of artificial intelligence.

The event will cover the latest breakthroughs in processors, memory, sensors and edge hardware fuelling next-gen AI, including insights from executives, technologists and engineers from across the globe.

Attendees will have the opportunity to engage in workshops and network through a virtual exhibition.

It’s great to see publications focusing on how AI is specifically driving change in the technology landscape, and we look forward to hearing insights from the event.

For further information on the invite, please click here.

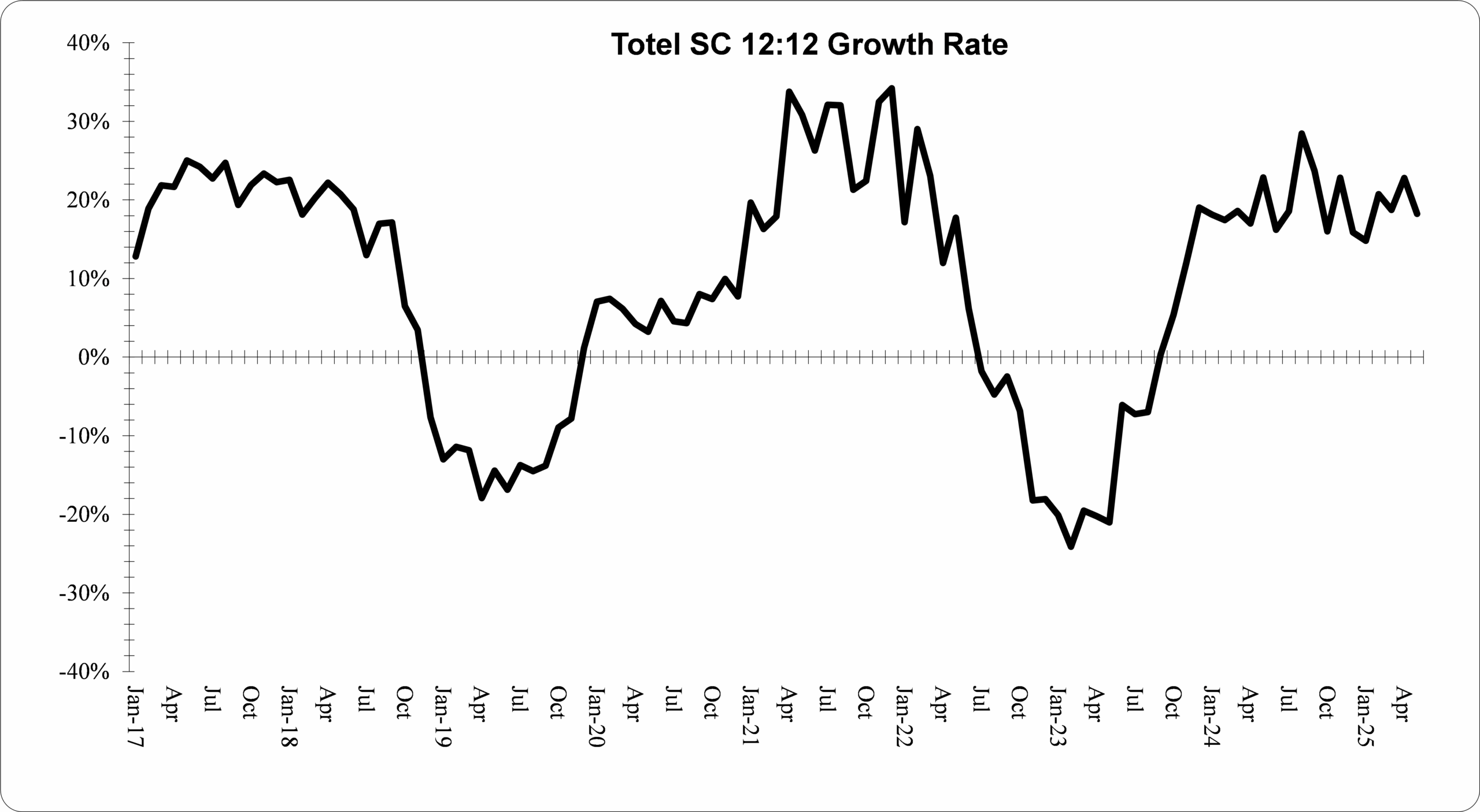

Future Horizons: September Semiconductor Update

We're pleased to announce this months excerpt from the Future Horizons Semiconductor Update. Check it out below for the latest industry insights:

Executive Summary

Annualised growth rates accelerated sharply in July, with Total Semiconductors growing 25.5 percent, up from last month’s 18.0 percent and May’s 18.5 percent, just three percentage points down from August 2024’s 28.5 percent cyclical peak.

Encouragingly, all three sectors performed well in July, with Total ICs continuing their lead as the prime industry growth driver at a robust 28.8 percent, significantly up from 19.9 percent in June and 21.4 percent in May, with Opto up 8.0 percent and Discretes up 6.9 percent, vs. last month’s 6.8 percent and 4.8 percent respectively.

Whilst the overall semiconductor market still showed a strong double-digit growth, the overall trend is flat, at around the 20 percent plus/minus level, varying from August 2024’s 36.2 percent peak to January 2025’s 14.8 percent low.

These peaks do not last forever, nor do they turn up, and we continue to expect to see this trend turn down in the coming months, as per past cyclical patterns, with the only uncertainty being as to when this will happen.

Forecast Update

Logic’s 37.2 percent annualised growth in July re-enforced its displacement of Memory, at 25.7 percent growth, as the IC sector’s star growth performer.

Logic’s growth was fuelled by a lacklustre 4.6 percent growth in units and an eyewatering 31.3 percent growth in ASPs, the sixth month in a row of 30 plus percent annualised growth.

As mentioned earlier, quite what is driving Logic’s strong growth is not clear but this time around, contrary to historical growth and competitive patterns, it is more in synch with Memory than the other product segments.

It is also ASP, not unit driven, which flies in the face of decades old semiconductor ethos (Moore’s law) and conventional economic (supply and demand) theory.

Clearly TSMC’s recent price hikes have been a contributory factor, along with the deep-pockets of the current spendthrift data-centre customers. Watch out for these prices to plummet once the broader IC market recovers and Moore’s second law kicks in … “The long-term IC ASP price is a dollar!”

Read The Full Report Here: https://www.futurehorizons.com/page/137/

In addition to its monthly report, Future Horizons is offering a one-day Silicon Chip Industry Workshop in London, giving a clear introduction to the semiconductor industry, from technology and manufacturing to markets and trends. Upcoming dates include 28 Oct 2025, 10 Mar, and 9 Jun, click here for more information on the workshops!

Future Horizons: August Semiconductor Update

This August, Future Horizon brings you fresh insights into the semiconductor industry. Dive into the latest market trends and outlook below.

Executive Summary

Annualised growth rates retreated again slightly in June, with Total Semiconductors growing 18.0 percent, down from last month’s 18.2 percent and April’s 22.9 percent and, whilst still in respectably high double-digit growth terrain, was still sizeably down from August 2024’s 28.5 percent cyclical peak.

All three sectors performed well in June, with Total ICs continuing their lead as the prime industry growth driver at a healthy 19.8 percent, albeit down from 21.2 percent in May and 25.2 percent in April, with Opto at 6.8 percent and Discretes at 6.2 percent, vs. last month’s minus 6.6 percent and plus 5.2 percent respectively.

Whilst the overall semiconductor market still showed a strong double-digit growth, the overall trend is flat, at around the 20 percent level, varying from August 2024’s 36.2 percent peak to January 2025’s 14.8 percent low.

These peaks do not last forever, nor do they turn up, and we continue to expect to see this trend turn down in the coming months, as per past cyclical patterns, with the only uncertainty being as to when this will happen.

Forecast Update

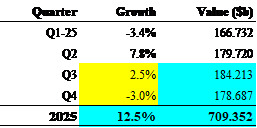

With the June results now in, at 7.4 percent overall quarter-on-quarter growth, the second quarter romped home a lot stronger than anyone predicted, either by earlier company guidance, which ranged from minus 10.7 percent (Kioxia) to plus 14.6 percent (SK Hynix), historical second quarter trends, or our 1.4 percent forecast.

2025 SC Growth By Quarter

(US$)

Source: WSTS/Future Horizons

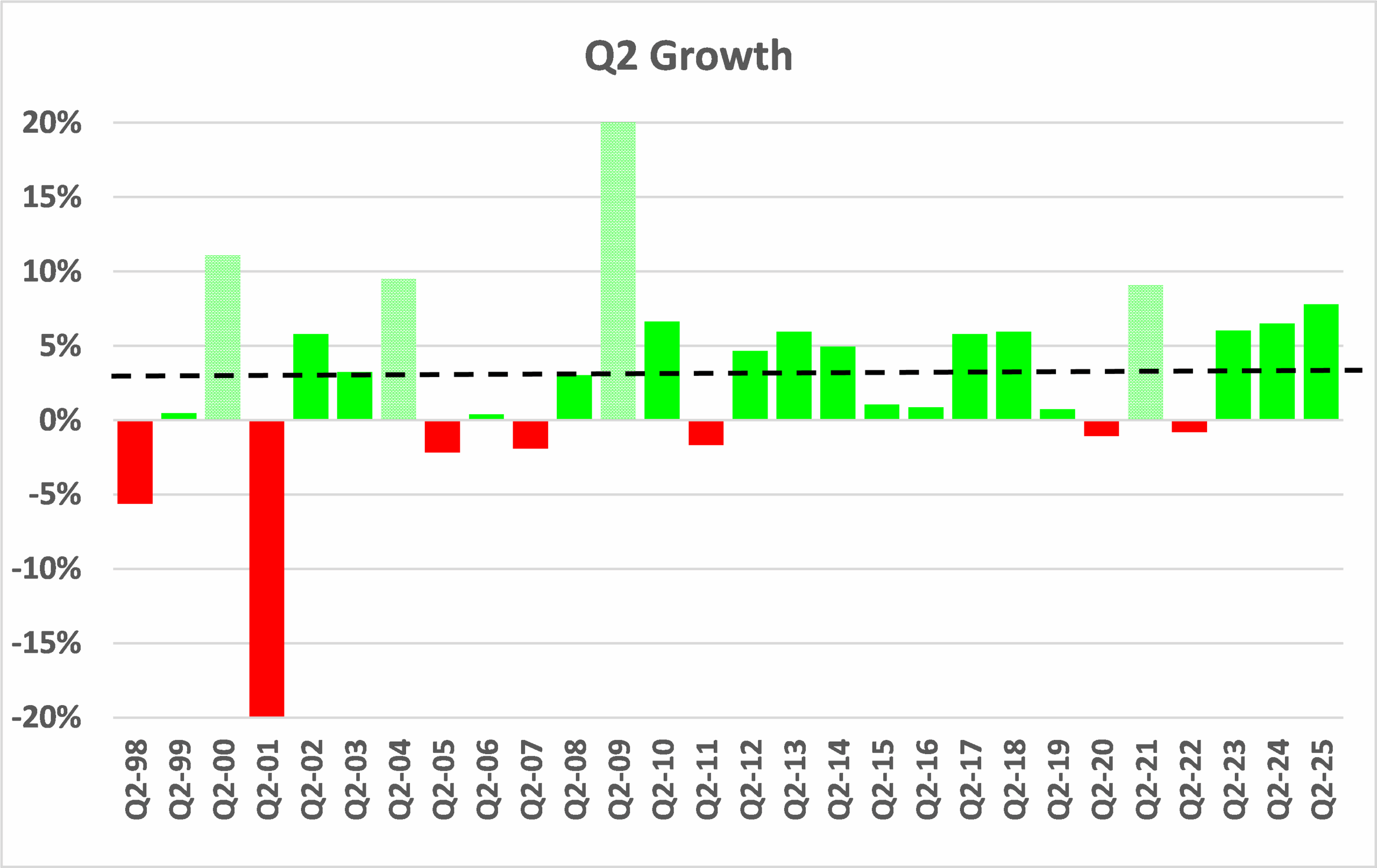

Q2 growth has averaged 2.9 percent since 1998, with only four results higher that Q2-2025’s 7.8 percent, namely in 2000, 2004, 2009 and 2021, each time at the height of a tight supply-side driven chip market boom, driven by capacity shortages and strong end-market demand.

Figure E11(b) – Q2 Growth Trend – 1998-2025

(Percent of US$)

Source: WSTS/Future Horizons

At the macro level, with the annualised sales of non-Memory ICs up 24.0 percent in June vs. 23.0 percent in May and 25.6 in April, and Memory ICs up 11.9 percent, vs. 17.5 percent in May and 23.8 percent in April, the annualised growth rates continue to paint a seemingly rosy outlook.

A deeper look under the hood shows a more confused and potentially bleaker picture. As has been the case since this current ‘boom’ started, the market has been driven by an economic anomaly of declining unit growth, resulting from the Covid-boom market shortages, but simultaneously increasing ASPs, in defiance of normal supply and demand economics and 70 plus years of chip industry history.

An even closer look reveals a deeply bifurcated market, one driven by the current AI boom and the rest, with the former comprising high-priced (for now) GPUs and exotic HBM products, both with near monopolist supply chains and deep pocketed, primarily data-centre infrastructure customers, immune to normal price-sensitive market pressures.

When your infrastructure investment programmes are costing hundreds of billions of dollars, the tens of thousand-dollar chip costs are lost in the noise. Not so if you are building a thousand-dollar smart phone or lap-top computer, or even a 100k dollar car.

Watch out for these high-prices ASPs to collapse, once the AI infrastructure boom runs its course, as it inevitably will. No boom lasts forever; all markets eventually saturate. In addition, pull-forwards are merely robbing future growth and stockpiles will eventually deplete.

As for the second-half year outlook, the current AI ecstasy, trade barrier risks, shipment pull-forwards and stockpiling are all clearly in play, which, along with broader economic concerns, have resulted in a potentially catastrophic atmosphere of heightened risk and uncertainty.

All this uncertainty, along with the on-going US tariff and trade flip-flops, is making the outlook for Q3 and the rest of the year increasingly unpredictable. The immediate key challenge is simply to ride and survive the current market tsunami.

At this point in the cycle, it would be wise to keep in mind Gordon Moore’s less revered second law, namely ‘Over the long term, the average IC ASP converges to $1’, or the fact the average revenue per square centimetre of processed silicon has been constant at US$ 9 since the advent if the IC.

If you are not selling these high-priced AI-related devices, you are currently living in a much different world, still bathed in recession, and more closely following the traditional industry trends.

Read The Full Report Here: https://www.futurehorizons.com/page/137/

Napier Shortlisted for 2025 Instrumentation and Electronics Awards - Vote Now!

We are delighted to share that Napier has been shortlisted for PR Agency of the Year in this year’s Instrumentation and Electronics Awards.

As a team we’re extremely passionate about the work we do, and strive to design, develop and deliver outstanding campaigns. Without our clients' support, we wouldn't have the opportunity to craft the incredible campaigns that allow our team to truly shine.

Voting is now open, and we’d like to ask for your support in voting for Napier. It only takes a few seconds to cast your vote, and can be done by:

- Clicking here to vote for Napier in ‘PR Agency of the Year’ category at the Instrumentation and Electronics Awards.

Congratulations to several of our clients including: Microchip, Tria, Vicor, Menlo Micro, Nordic Semiconductor and many more, who have also been shortlisted for award categories this year.

Best of luck to all the nominees, we’re looking forward to celebrating with you at the ceremony later this year.

Vogel Launches New Aerospace & Defence Digital Platform

Vogel Communications Group has announced the launch of their new digital aerospace and defence platform.

The new site launched on 1st July and is designed to support better visibility and communication in Europe's fast-growing aerospace, defence and security sectors.

As an international platform, Vogel's focus will span the entire defence industry chain, from advanced engineering and manufacturing to avionics, electronics, software, and digital transformation. The site also explores critical topics like security systems, as well as emerging trends and market dynamics that are defining the future of the industry.

Vogel’s new platform is a smart move and the platform is making it easier for people across the industry to stay informed, connected, and ahead of the curve!

Future Horizons: July Semiconductor Update

This month, we bring you the July edition of Future Horizon’s semiconductor report. Explore the latest insights into the current market outlook below.

Executive Summary

Annualised growth rates retreated slightly in May, with Total Semiconductors growing 18.2 percent, down from last month’s 22.8 percent and March’s 18.7 percent and, whilst still in double-digit growth terrain, was still sizeably down from August 2024’s 28.5 percent cyclical peak.

Total ICs continued to be the star sector performer, at a healthy 22.9 percent, albeit slightly down from 25.1 percent in April, with Opto at minus 5.5 percent and Discretes at plus 4.8 percent, vs. last month’s plus 16.0 percent and plus 5.5 percent respectively.

Whilst the overall IC market still showed strong double-digit growth, the overall trend is flat, at around the 20 percent level, varying from August 2024’s 36.2 percent peak to January 2025’s 14.8 percent low.

Monthly Annualised SC Growth Rate Trends

(Jan 2019-May 2025 – Percent of US$)

Source: WSTS / Future Horizons

We still expect to see this trend turn down in the coming months, as per past cyclical patterns, with the only uncertainty being when this will happen.

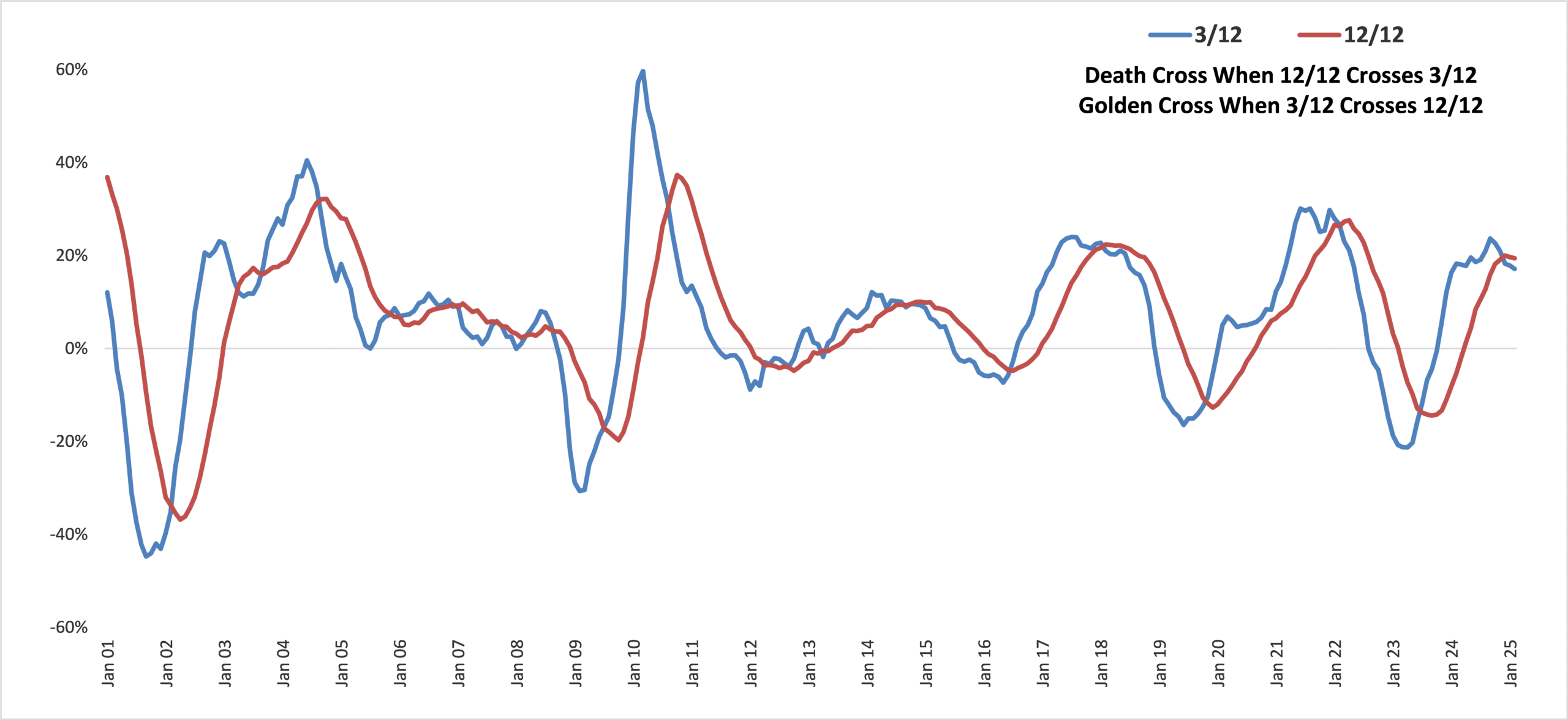

Market Growth Indicators

The 3/12 curve fell back slightly in May, to 19.8 percent, vs. 20.6 percent in April, 18.8 percent in March and 17.1 percent in February, whilst the 12/12 curve increased to 20.1 percent, up from 19.6 percent in April and March, more in keeping with the curve having reached its traditional cyclical peak.

As a result, the gap between the two curves reversed from last month’s plus 1.0 percentage points to minus 0.3, pushing the growth momentum indicator back into Death Cross territory.

Given the depressed state of the non-AI market sectors, the worsening overall global economic outlook, the still on-going excess inventory and massive overcapacity, April’s excursion into calm waters looks likely a short-lived gain before moving back into the storm, with the length and timing of the transition depending on how much longer the current AI infrastructure boom prevails.

Disaster Waiting To Happen

April’s total CapEx spend as a percent of semiconductor sales was 19.4 percent in April, vs. 22.6 percent and 18.4 percent in March and February respectively. The long-term safe-haven trend is 14 percent.

The equivalent numbers for Wafer Processing (Front-End) Equipment CapEx spend were 16.4 percent, 19.0 percent and 13.0 percent respectively, with the overall trend again well above the 11.0 percent long-term safe-haven trend.

The industry is continuing to stubbornly over-spend on CapEx, with no sign yet of any attempt to cut back, let alone move back below the trend line to compensate for the last two-plus years of excess capacity investment.

The current trend is parallel to the massive over-investment euphoria in the mid-1990’s memory and 2000’s dot.com booms.

We should all know by now how this scenario will end, we just never know when, but past experiences are more often forgotten than learned, allowing irrational exuberance and bad practices to prevail.

Greed always overcomes fear before the whole thing goes ka-boom.

A timely reminder to reflect on Albert Einstein’s quote “Insanity is doing the same thing over again and expecting a different result?”

Read The Full Report Here: https://www.futurehorizons.com/page/137/

Electronic Notes Launches Online Shop

Electronic Notes has announced the launch of its online shop covering a range of products from vintage valve mugs to Morse code mouse mats, and op-amp circuit mugs and coasters.

The launch of the online shop was built with electronics engineers in mind to provide products that engineers would want, rather than just reproducing logos. The shop is now live and can be accessed here.

It's great to see publications taking a slightly unusual route, extending their offerings and developing products that can be used by engineers and enthusiasts alike.

Certified for Success: How Our Digital Team Drives Success

In today’s B2B marketing landscape, success relies on more than creativity, it demands mastery of platforms and developing your skills. That's why our digital team undertake comprehensive training, gaining certifications that help boost their digital skills and knowledge.

As an employee owned agency we like to invest in our team, so what certifications does our digital team uphold?

-

Google Ads & Google Analytics (UA & GA4)

Every member of the digital team uses these tools to understand audience behaviour, optimise campaigns and drive ROI. -

LinkedIn

A platform which can be leveraged for targeted outreach, brand awareness and thought leadership. This is often an essential platform for several of our clients' campaigns. -

SharpSpring

Our teams expertise in automation workflows and email nurturing keeps us agile and effective in mid‑market campaigns. -

Oracle Marketing Cloud Academy

Our Head of Digital, Helen, supports the team in delivering scalable enterprise campaigns with precision. -

HubSpot SEO

A strategic approach to content optimisation, keyword tracking and SEO structure ensures our owned channels perform. -

Salesforce Marketing Cloud (Pardot)

Combining automated lead scoring with advanced campaign reporting helps support our clients' digital growth in the B2B landscape. -

Adobe Suite (AEM, Marketo, Analytics)

From content management to analytics, we ensure campaigns are both creative and measurable.

At Napier, our strength comes from combining tools, training and teamwork. Up-to-date certifications and weekly training sessions keep our team both well informed on digital developments and ahead of the curve. As a result, our team can deliver smarter strategies and, in turn, better results for both Napier and our clients.

Future Horizons: June Semiconductor Update

This month, we present the June extract of the Future Horizon's semiconductor report. Find out more about the current outlook of the market below:

Executive Summary

Annualised growth rates rebounded in April, with Total Semiconductors growing 22.8 percent, up from last month’s 18.7 percent number but still down from August 2024’s 28.5 percent cyclical peak.

Total ICs continued to be the star sector performer, at a healthy 25.1 percent growth up from 22.6 percent in March, with Opto at plus 16.0 percent, vs. minus 3.5 percent in March, and Discretes up 5.5 percent vs. March’s 0.9 percent decline.

Whilst the overall IC market still showed strong double-digit growth, the overall trend is flat, at around the 20 percent level, varying from August 2024’s 36.2 percent peak to January 2025’s 14.8 percent low. We expect to see this trend turn down in the coming months, as per past cyclical patterns.

Annualised growth rates are, however, just one side of the coin. Our preferred measure is the month-on-month revenue growth trends, which we believe are a more accurate reflection of the overall industry health.

From a market perspective, growth is still very much AI infrastructure driven, with the broader, more general, markets yet to recover from the post-Covid downturn. A worsening global GDP outlook could trigger a global recession.

This combination of circumstances is a perfect storm on steroids.

- GDP growth has been revised down, from 3.3 percent to 2.8 percent;

- There is no rebound yet in sight for a rebound in IC unit shipments;

- ASP are all falling, except for some yet unclear reason in Logic, and:

- Excess capacity abounds and is poised to get worse.

The broader industry dynamics are dreadful. Under normal industry conditions, short of a major geo-political or natural disaster crisis it doesn’t get much worse than this.

Read the full report here: https://www.futurehorizons.com/page/137/

Mark Your Calendar: ECF25 Returns September 2025

On September 16th 2025, the Embedded Conference Finland returns for its 7th year, taking place at Maria 01 in Helsinki.

Recognised as one of the leading events for electronics professionals in Finland, the event provides a platform for designers, corporate buyers, business leaders, and those interested in embedded technology to network and share the latest industry developments.

This year's agenda is packed with keynote speeches, technical presentations, and a panel discussion featuring industry insights. More details around the specific topics are expected to be released soon.

Registration for visitors is free, and you can register by clicking here.

The Ojo-Yoshida Report Has Rebranded!

The Ojo-Yoshida Report, a well-known voice in tech journalism, has rebranded as TechSplicit, a brand dedicated to exploring the global high-tech landscape, and the intended and unintended consequences of innovation and decisions within the sector.

Led by founder and Editor-in-Chief Bolaji Ojo, TechSplicit will investigate the greater implications of technology on markets, policy, economies, and society.

Joining Ojo in a new leadership role is Mike Markowitz, now Editor-at-Large. They lead an editorial team with over a century of combined experience in semiconductors and international tech.

TechSplicit will also expand its content offerings with a new podcast series and virtual summits on some of the most critical and high-growth areas of the industry including AI, semiconductors, power, and electronics lifecycle management.

It’s interesting to see this rebrand, as Junko Yoshida moves on from the news platform. We look forward to seeing how the publication and its content evolves with this change.

Meet Napier's Head Of Content: Q&A With Phil Gibson

‘This year marked 10 years since I first started on this journey, and I haven’t really looked back.’

Content is often at the heart of every campaign. At Napier, we often present our campaigns as 'content-driven', whether that be in a traditional PR format like articles, or a digital marketing format through LinkedIn or Google ads.

I recently chatted with Napier's Head of Content, Phil Gibson, who shared his journey into the industry and how our content creation capabilities support our clients.

Could you begin by telling me a bit about your time at Napier?

No good story would be complete without some sort of love interest, and mine is no exception.

It’s 2014, and I’m eking out a (very) modest living doing freelance copywriting by day, and pulling pints by night. Then I met a girl. The problem was that I lived in Guildford, and she lived in London. So on a Friday night, I would finish my shift at the pub and charge up the A3 in my tiny Peugeot 106 to spend the weekend with her, before coming back on Monday morning for my next shift at the pub. I kept this up for nearly a year, but also knew I had to find something more permanent (and better paid) to allow me to move in with my then-girlfriend.

Enter Armitage Communications, which in 2015 offered me a job right at the bottom of the ladder as a Junior Account Executive. Crucially, it enabled me to move up to London and start building a proper career for myself. A year later, my girlfriend became my fiancée, and in 2017, she became my wife (which bizarrely made headlines around the world).

In 2019, Armitage Communications was bought by Napier, which makes me (along with Ed, Helen and others) part of the Armitage alumni. By this time, I had progressed up the ladder from Junior Account Exec to Account Exec, and then onto Account Manager. But I was still known as a specialist copywriter, and it was only after Napier took us over that I was allowed to really spread my wings and focus on what I was best at – content.

Upon starting your agency career, what is the one piece of advice that stuck with you?

That there’s no such thing as a stupid question. It’s natural to feel scared of getting things wrong and receiving a telling off from the higher-ups. But it’s always better to check first and do something right than to get it wrong and have to do it again.

In relation to content specifically, a big part of my job is interviewing client personnel to either get a handle on the technical nuances of a story, or to add some personality and flavour, or both. I find that even in this environment, there are still no stupid questions. These people simply love talking about what they do, particularly when it’s to someone who’s genuinely interested, like I am – and so it’s incredibly rare that anyone is rude or impatient with me. I’d like to think that they also find it rewarding when that lightbulb moment occurs, and I suddenly get it.

What was your journey to head of content like?

So, about a year after Armitage became Napier, I was given a choice of what sort of specialism I wanted to pursue, between account management and content. Naturally, I chose content. With that said, because I can do both, I still manage some accounts of my own. And I’d like to think that because I’ve got a foot in both camps, I can bring a unique perspective when it comes to advising or suggesting ideas to colleagues and clients alike.

Today, I’m Head of Content Development, and I essentially run the content department at Napier. As well as making sure we’re always delivering content of the highest quality, I also manage both our in-house and freelance resources to make sure that we always have capable writers for every sector we operate in.

Have you always wanted to be a technical writer? How did you fall down this path?

I always knew I was good at writing and the English language, and so I hoped that I would end up using those skills somehow. But this agency (and its previous incarnations) found me, rather than me actively seeking out a role in B2B technical writing from the outset.

With that said, this year marked 10 years since I first started on this journey, and I haven’t really looked back.

What is a regular day like for the Head of Content Development?

A typical day for me will often have fewer meetings compared to others, but that’s because I need time to actually write content for clients. We’ve built a content team here that can handle pretty much anything, but I’ll often take on some of the complex and high-value projects myself to ensure they’re delivered to the highest quality.

When I’m not writing, I’ll often be in sourcing calls to interview client personnel, or discussing content resource planning with colleagues, or catching up with freelancers to brief them, provide feedback, and make sure that projects are staying on track.

Any writer will tell you that reading the work of others is vital to improving your own writing. Luckily for me, the content pipeline at Napier is so voluminous and formidable that there are always opportunities for me to look at what others are doing and try and find ways to incorporate the best ideas and approaches into my own work.

How can content creation support our clients?

I may be biased, but in my view, content is EVERYTHING. You can’t have a marketing campaign without content to underpin it. To speak to customers effectively, you first need a message worth listening to. At Napier, we have a vast range of marketing tactics that we implement, and the majority of them rely on having compelling content that engages your audience.

At the same time, I don’t believe in content for content’s sake – it needs to be outcome-driven. That’s where Napier’s 4-step process comes in useful to make sure that content generation is not just for the sake of it, but created to complement and drive the broader marketing strategy.

What is one piece of advice you give to new starters at Napier?

Probably the same advice that I received myself: There’s no such thing as a stupid question. That’s one of the cool things about Napier, that everyone is always willing to help each other out.

What is a project you're most proud of and why?

With 10 years under my belt, there’s quite a lot to choose from. The most memorable was probably when I got sent to Zurich at short notice to do some on-camera interviewing. Even though I spend most of my days interviewing people for articles and white papers, I’m more of a writer than a broadcaster by trade, and so this was somewhat out of my comfort zone. It’s one thing reading your questions off the page or screen, but having to completely freestyle it on camera, and look the part while you’re doing it, was a different beast altogether.

The videos that came out of that shoot were extremely high quality, which made it a rewarding project to be part of. And the whole experience of going out there, managing the client and the film crew, not to mention having to deliver on-camera, was something I found very exhilarating.

What do you feel your strongest quality is?

When you do what I do, you have to be a good listener, and you have to be able to get on with people. Sometimes when you’re interviewing people, it’s clear that they just don’t want to talk to you. Perhaps they’re busy, or they’re having a bad day, or they just don’t understand why they’re there. Sometimes, just asking the right question in the right way, or knowing when to let the conversation meander and when to bring it back, can help to open the floodgates and turn what might have started out as a difficult interview into a genuinely fun one.

What was your dream job growing up, and why?

When I was a kid, I wanted to be something different every day of the week. And I mean that quite literally: I wanted seven different jobs that I’d do for one day each week, so on Monday I’d be a train driver, Tuesday a footballer, Wednesday a bricklayer (don’t ask), and so on. Even from a young age, I always loved being creative and telling stories, and so one of those jobs, believe it or not, was “Writer”.

I may not have managed to achieve all seven in my life (although there’s still time), but to get to do one is definitely a win.

Entries For The Elektra Awards 2025 Are Now Open!

Entries are now open for the Elektra Awards 2025, which will take place on Tuesday, 9th December at the Hilton Bankside in London.

Now in its 23rd year, the awards feature 18 categories, with a new addition for 2025, the Neurodiversity Product Design Award.

The awards recognise and honour innovations and accomplishments by those shaping the industry, from start-ups to enterprises, and experienced electronic engineers.

Be sure to enter before the final deadline of 13th June 2025.

The Brightspark Awards entry is also now open. Celebrating promising young professionals (30 years old or under) in the electronics industry, the awards recognise those already making a difference in the first years of their careers, or those who are still studying but showing promise to become the leaders and innovators of the future.

Guest Blog - Kay Petermann's View On Canton Fair Visit In China

We were delighted to receive a guest blog from Kay Petermann, Editor of IEN DACH, who discusses his visit to the Canton Fair in China and his view on the event:

The opportunity to attend the 137th session of the China Import and Export Fair is a new and interesting experience for me. It is new after nearly twenty years of attending European B2B events.

Having attended European shows in the broader factory automation environment since I joined a B2B publishing company in the summer of 2006, this week has opened a new chapter in my career. I travelled to Guangzhou, China to attend the 137th Canton Fair as editor of IEN Europe. With its 55 exhibition sections and 172 product zones, this is the most horizontal event I have attended in my professional life; even the Hannover Messe, one of Europe's major spring events each year, has a fairly vertical selection of industries compared to this. Certainly, one of the first things you notice is the high level of internationalization, with buyers from more than 210 countries and regions.

China's industrial innovations in batteries, photovoltaics, digital technologies and intelligent manufacturing are represented with a focus on advanced technologies and green solutions.

One of the new highlights of the show is the Service Robots Zone, which showcases the latest developments and innovations. From manufacturers of joints and grippers that work like a human hand, to cobots and mobile robot units for the agricultural industry, harvesting fruit or vegetables such as tomatoes, they are all there. And that is not all. You can also find innovative designs for surveillance and detection, used for monitoring tasks in hazardous industrial areas, or for finding and rescuing people in a fire zone or after a natural disaster.

Another trend you can see, as at the European events, is that robots are becoming humanoid. When it comes to service and human-machine interaction, these design features clearly make sense, as they allow people to interact with a friendlier-looking machine. The benefits in industrial and manufacturing environments remain to be proven. However, a few years ago, nobody would have thought that a 20-inch multi-touch interface would be the way to go for machine operation, and you know what customers are demanding in terms of HMIs today.

With the growing investment in China's robotics sector over the next 10 years, the size and versatility of the Service Robot Zone at the show will certainly grow to the next level. I really hope to come back in the coming years to see this transformation and innovative ideas live and in action.

Future Horizons: May Semiconductor Update

We're happy to share this month's extract from the Future Horizons May report on the semiconductor market. Explore the latest market perspective and informed insights below.

Executive Summary

Annualised growth rates tapered off in March, with Total Semiconductors growing 20.6 percent, down from last month’s 20.7 percent number and August 2024’s 28.5 percent cyclical peak.

Total ICs continued to be the star sector performer, at a healthy 24.8 percent growth up from 24.1 percent in February, with Opto at minus 3.5 percent, vs. minus 2.3 percent in February, and Discretes dropping back into negative growth territory, at minus 0.9 percent, following last month’s short-lived excursion into positive annualised growth.

Whilst the overall IC market still showed strong double-digit growth, the overall trend is still one of decline, a downward trend that started from August 2024’s 36.2 percent peak seven months ago, Figure E1(a). We do not expect this trend to turn up anytime soon.

Annualised growth rates are, however, just one side of the coin. Our preferred measure is the month-on-month revenue growth trends, which we believe are a more accurate reflection of the overall industry health.

Worryingly, March saw monthly sales shrink 7.5 percent vs. February, reversing both last month’s growth and more severe that January’s 5.6 percent decline.

Even more worryingly, this decline was broadly spread across all IC sectors and the fact that March, being the last month of the quarter, is seasonally usually quite strong.

The key factor driving the 2025 semiconductor market continues to be an apparently insatiable AI data center server demand, the key factor that drove most of the 2024 market growth. So far, this sector shows no sign of slowing down, with the best-case scenario anticipating a strong, but significantly lower growth rate in 2025.

The outlook for the other key markets, such as smartphones, PCs, automotive and industrial, remains weak, and are unlikely to compensate for any slowdown in the AI-infrastructure deployment.

The global economic outlook for 2025 is not strong, especially with the uncertainty of the threatened U.S. increased tariffs on imports on global trade and other countries promising retaliatory actions.

The chip industry needs a strong global economy to thrive … we expect to be significantly downgrading our January 2025 forecast from 15 percent to single digits at our Spring Semiconductor Industry Outlook Webinar on May 13.

You can read the full report here: https://www.futurehorizons.com/page/137/

Editor of Power Electronics News Starts Two New Series!

Maurizio Di Paolo Emilio, the Editor of Power Electronics News, recently announced the launch of two new video series, Power Up Circuit Lab and ESD. These new series connect engineers, students, makers, and professionals in power electronics and embedded design. Using short videos, Maurizio engages with viewers to explore development boards, power modules, and test tools with clear, practical coverage of basic and advanced topics. He aims to use these series to bring together the industrial sector and maker communities.

It's no secret that journalists are extremely busy, and in such a fast-paced and at times chaotic media landscape, it is always impressive to see journalists like Maurizio creating and developing new ways to interact and engage with individuals within the industry. We look forward to seeing the series progress, educate and grow!

Future Horizons: April Semiconductor Update

We present this month’s excerpt from Future Horizons’ April report on the semiconductor market. Read on to discover the latest insights and outlook for the industry.

Executive Summary

Annualised growth rates turned up in February, with Total Semiconductors growing 20.7 percent, up from last month’s 14.8 percent, but still down from November 2024’s 22.8 percent high and August 2024’s 28.5 percent cyclical peak.

Logic continued to be the star sector performer, at a healthy 35.8 percent growth, up from 29.7 percent in January, with second-place Memory growing 26.6 percent, down from 29.9 percent in January.

Analog ICs moved back into positive territory in February, growing 8.8 percent, vs. minus 0.4 percent in January, as too did Total Micro, growing 2.6 percent up from last month’s minus 0.4 percent.

The overall IC market ended up growing 24.1 percent year-on-year, up from last month’s 19.4 percent number but significantly lower than November 2024’s 29.5 percent growth and August 2024’s 36.2 percent peak.

The overall trends, however, are still indicating retrenchment vs. recovery, having been now on a downward trend for the last six months. We do not expect this trend to turn up anytime soon.

Annualised growth rates are, however, just one side of the coin. Our preferred measure is the month-on-month revenue growth trends, which we believe are a more accurate reflection of the overall industry health.

Thankfully, February saw monthly sales grow 6.5 percent vs. January, reversing January’s 5.6 percent, December’s 8.7 percent and November’s 8.7 percent decline.

Even more thankfully, this growth was broadly spread across all IC sectors bar Analog, which is still gripped in recession.

Market Growth Indicators

December 2024 saw the industry move into death cross territory, with the 3/12 curve declining further in February, to 17.1 percent, vs. 17.9 percent in January 2025, 8.2 percent in December 2024, and September 2024’s 23.7 percent peak.

At the same time, the 12/12 curve continued its gradual decline, at 19.4 percent vs. 19.7 percent in January and its 20.2 percent December cyclical peak.

As a result, the gap between the two curves widened slightly to 2.3 percentage points, vs. 1.8 percentage points in both January 2025 and December 2024.

WW SC Growth Momentum Indicator

(Jan 2001-Feb 2024 – Percent of US$)

There are three potential scenarios now in play, depending on how the 3/12 curve plays out.

Scenario 1: The 12/12 curve continues its cyclical decline but the 3/12 curve flattens off heralding a modest Golden Cross sometime in the mid- to late-2025, as in 2018.

Scenario 2: The 12/12 curve continues its cyclical decline with the 3/12 curve following its more typical decline trajectory, paving the way for an extended industry walk in Death Cross territory throughout the whole of 2025, as in 2014.

Scenario 3: The 12/12 curve turns back up whilst the 3/12 curve continues its decline, heralding a much stronger Golden Cross sometime in the first half of 2025, as in 2003.

At this juncture, it is hard to predict which scenario is most likely but, if the broader chip market continues its slow and modest recovery and the current AI-inspired boom does not crash and burn, then Scenario 1 is the most likely outcome.

You can read the full report here: https://www.futurehorizons.com/page/137/

IEN Europe Marks 50 Years

Congratulations to IEN Europe, which is celebrating 50 years of covering the industrial engineering industry.

From originally building connections through postcards, the publication evolved with the development of the digital age, launching the TIMLab Customer Zone. The online platform encourages communication between both sides of the industry, showcasing IEN Europe's commitment to educating industry suppliers and consumers.

With five decades of industry experience, the publication has and continues to actively explore emerging trends, technologies, and challenges that have defined the industrial landscape across the last 50 years.

Congratulations to IEN Europe on this monumental achievement. We look forward to witnessing the innovation and progress to come!

MVPro Media Launches North American Website

MVPro Media, the UK-based B2B publishing company specialising in machine vision and industrial image processing, has recently announced the launch of its North American website.

The new site will be a resource for those based in the US and will support the navigation of the evolving opportunities in the machine vision space. Focused on the future of industrial innovation, MVPro Media is for industry professionals, design engineers, manufacturing, production and quality control decision makers interested in optimising efficiencies.

It's always great to see the expansion of a publication, and the MVPro website in North America will be a great opportunity for the publication to showcase key insights, news and emerging technologies and products to its target audience in North America.

Electronics Weekly Launches Monthly Review Issue

Electronics Weekly has recently announced plans to introduce a monthly publication, replacing the current hybrid-news publication. Entitled, Electronics Weekly Review, the magazine will include thought leadership content and technical stories picked by the editorial team.

Readers will have access to exclusive worldwide electronics news, including market updates, the month’s top international News and analysis, and a distribution updates segment.

The new magazine will cover all areas of the electronics industry, from an emerging technology trends editorial section, to a new Education and STEM section which will highlight initiatives and projects to increase engagement in STEM.

Interviews with company leaders, upcoming members of the industry, inspiring individuals and entrepreneurs will also be featured, alongside a Blog Spot which will highlight the best of Electronic Weekly’s blogs.

“The investment in print means that the Review magazine is a true heavyweight with an arresting cover and strong editorial content,” said Electronics Weekly’s Editor, Caroline Hayes.

“The monthly frequency will allow journalists to provide a broader perspective of the industry, complementing the daily news we provide, and also present longer-form articles available exclusively to subscribers in a print or digital issue”.

It’s been a busy month over at Electronics Weekly HQ as they have also launched a new podcast, CHIIPS (Caroline Hayes’ Industry Insights Podcast). The podcast will feature discussions with industry leaders and personalities on topical subjects within the electronics industry.

The first edition of Electronics Weekly Review is due for distribution April 24th. We look forward to reading the new magazine and we wish the team at Electronics Weekly the best of luck with the launch!

Electronic Specifier Shines At Embedded World

Electronic Specifier partnered with #women4ew to co-host this year’s Women in Tech Forum at embedded world 2025. Held on 13th March in Nuremberg, Germany, the event brought together professionals from across the embedded systems sector to celebrate, inspire, and empower women in technology.

The forum featured an inspiring line-up of speakers who shared their experiences and insights on navigating careers in the tech industry. Helen Duncan, CEO of Blueshift Memory, delivered an engaging keynote, offering attendees a refreshing perspective on career progression. Sakshi Madaan, Product Manager at Anders Electronics, followed with her talk, ‘The Power of Perspective: Big-Picture Thinking to Drive Innovation’, which encouraged attendees to embrace strategic thinking as a driver for innovation.

The event also featured a panel discussion, moderated by Managing Editor of Electronic Specifier, Paige West. Joining the keynote speakers on the panel were Angela Raguse of Fraunhofer IIS, Stefani Eisele of Altera, and Nadja Eder of SchuhEder Consulting.

The panellists shared their experiences and discussed the evolving role of women in embedded systems, highlighting the importance of community and collaboration in fostering inclusive environments.

The forum concluded with a networking session, providing attendees the opportunity to connect, share experiences, and build lasting relationships.

The Women in Tech Forum has firmly established itself as a key event at embedded world.

Electronic Specifier also announced the winners of its Electronics Excellence Awards at embedded world 2025, of which entries were judged by a panel of thought leaders and electronics specialists.

The following companies took home the awards including:

- Power: Nordic Semiconductor – nPM2100 PMIC

- Electromechanical: NXP – i.MX 94

- Test & Measurement: Dukosi – DKCMS

- Passive: Swissbit – Security Upgrade Kit

- Software: Silicon Motion – SM2264XT automotive SSD controller

Congratulations to all the winners!

Engineers Trust Experts Over AI – What This Means for Marketers

The 2025 State of Marketing to Engineers report conducted by TREW Marketing, GlobalSpec, and Elektor International Media makes one thing clear: engineers look less at AI-generated content and more towards publications. Their recent survey of more than 1,000 engineers found that 67% rate their trust in AI at 5 or below on a 10-point scale, while 70% rarely or never use AI to evaluate vendors when making buying decisions.

As a result, 86% look for third party sources they know they can trust, including supplier websites, technical publications, and third-party reviews.

What can marketers learn from this?

That engineers, in particular, value authoritative voices.

The loyalty between engineers and individual authors, trade journalists and experts has never been more important, and is growing, in large part because we don’t believe that AI can replace human knowledge and expertise.

So, AI isn’t likely to kill journalism or marketing any time soon. But, what can marketers do to prevent it? The answer is simple: focus on building relationships with respected industry figures and publish verifiable content about products and services through their reputable outlets.

If you want to learn more about the survey’s findings, experts from Elektor International Media conducted a webinar on the 2025 State of Marketing to Engineers, which is available on demand here.

The State Of Publishing: An Editor’s Lament

This month, we would like to feature a guest blog from an anonymous editor who reflects on how their once fulfilling career has changed over time:

I’d been looking to break into technical journalism for some time, so when I won my first editorship in an aerospace manufacturing title, I was like an energetic rookie pilot on his first mission.

There was so much to comprehend in terms of the sheer size and scope of a competitive and vibrant industry that in terms of design and manufacturing technology, it knew no bounds.

The latest composite aerostructures, increasing integration of embedded electronics and environmental initiatives meant technology breakthroughs happened nearly as regularly as flights in and out of our busiest airports.

I travelled the world, met and interviewed interesting spokespeople who continually demonstrated that the industry was a hotbed for evolving innovative product designs – it was full of creative people thinking not only of the here and now, but of the aircraft of tomorrow.

However, things have come to a pretty pass when my role has now been reduced to the point where I’m simply editing ‘puff’ copy to keep the advertisers happy. The rise of social media, sales erosion, and swingeing financial cutbacks means it really has become a race to the bottom for the entire trade press publishing industry.

And now the sales tail is truly wagging the editorial dog. ‘Why did you travel to see [insert name/location here]? They never advertise’, wails the sales director. Oh, I’m sorry – I thought my job as editor was to source cutting-edge news/feature articles that would interest our readers?

Ah, the readers. I’d forgotten about them, hadn’t I?

I miss the press trips, the crazy food, the airport lounges, the press gifts, and most of all I missed the friendships and laughs. Nowadays, I’m made to feel like I’m something you shouldn’t step in, judging from sour-faced looks I get at some exhibitions. I find myself almost grovelling.

Whilst you can’t exactly call me a salesman, I’m now considered more of a ‘brand ambassador’ than an editor. Apparently, us editors now have ‘clients’. Oh, yes! The editor’s little black book of contacts doesn’t belong to the editor anymore – sales are privy to it too, so lead us to your ‘client’.

What was that old Reithian BBC saying? Inform, Educate and Entertain. The bottom line is, I don’t feel like I’m needed anymore.